{kind=link}

It’s rare to see a macroeconomics experiment play out in real time in the way we are seeing it right now in Japan and Europe. Prime Minister Shinzo Abe has embarked on aggressive measures to stimulate Japan’s long-moribund economy since he took office in December, and the result so far has been strong growth — and, perhaps, liftoff after a triple-dip recession. Europe, on the other hand, remains mired in the muck of austerity and economic contraction.

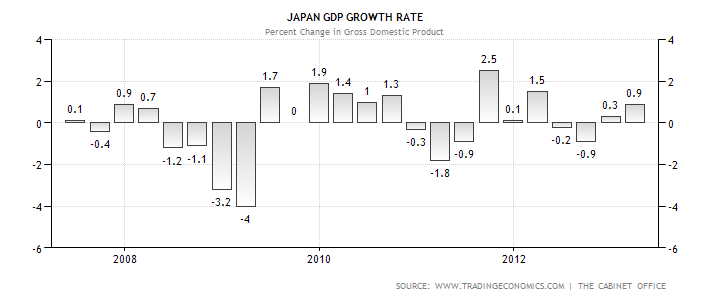

To briefly recap Japan’s economic woes: the Japanese economy has been largely stagnant for the last two decades. Since the financial crisis in 2008, it has gone through three bouts of negative growth. Its economic output per person — GDP per capita — was actually lower in 2012 than it was in 2008.

In the economics profession, this is what they refer to in technical terms as “not good.”

However, Japan’s economy surged in the first quarter of this year, growing at an annualized rate of 3.5 percent. For its part, the Abe administration credits a three-pronged economic strategy, dubbed Abenomics: “unprecedented monetary stimulus, a big boost to government spending, and structural reforms designed to make Japanese industry and institutions more competitive.”

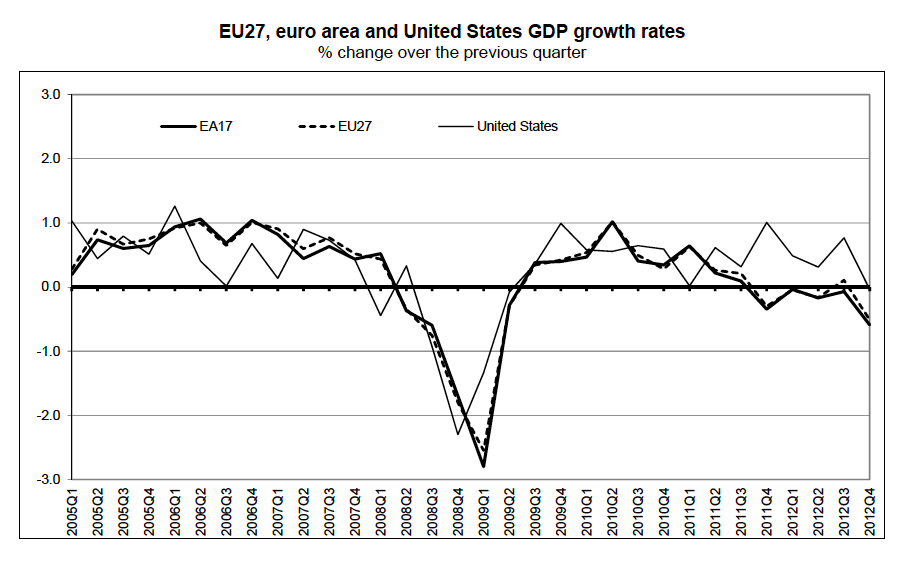

Then there’s Europe, which refuses to shift away from austerity. Its economy shrank for the sixth consecutive quarter — its longest downturn since World War II.

“The real economy is responding [in Japan],” said Adam S. Posen, president of the Peterson Institute for International Economics in Washington. “The last five, six months, there’s been a mini consumer boom. All the things that people said could never happen in Japan have turned around.”

He added: “Japan’s central bank is supporting recovery, and it’s working. The European Central Bank is supporting stagnation, and it’s working.”

Some in Europe understand that austerity is the problem, not the solution. Unfortunately, that “some” does not include the people making the decisions:

“The elites in Europe don’t learn,” said Stephan Schulmeister, an economist with the Austrian Institute of Economic Research. “Instead of saying, ‘Something goes wrong, we have to reconsider or find a different navigation map, change course,’ instead what happens is more of the same.”

Schulmeister added that German Chancellor Angela Merkel — austerity’s champion and the one person who could push Europe to change course — is “not willing to learn” the lesson offered by Japan’s recent switch from contraction to growth.

Apparently, Europe (read: Germany) sees austerity as a kind of “morality play” whereby the profligate must suffer for their sins. And yet the people most responsible for Europe’s economic crisis are the ones suffering the least from austerity. Although unemployment in the euro zone reached a new high in March, you don’t see bankers and politicians on the unemployment line. What’s really immoral is an austerity policy that punishes the innocent while one guilty party bails out the other.

Regardless of who is hurting, austerity is simply not always the best way to achieve its supposed goal: reducing government deficits. As Europe reminds us, it prevents recession-battered economies from growing. The alternative is to prime the economic pump by having governments engage in fiscal and monetary stimulus. When economies grow under this approach, Keynesian economists like Paul Krugman argue, governments collect more in the way of revenues, straightening out their finances faster than they would by reducing their spending.

Once a country’s economy is again operating at capacity, government should cut spending — and increase taxes on those who can afford it — in order to deal with the problem of deficits in a balanced, moral way that neither grievously harms the economically vulnerable nor sacrifices the long-term investments by government that are necessary to further growth over time.

The lessons to be drawn from the recession are counterintuitive. The dominant morality tells us to tighten our belts and save up. But if the government as well as the private sector hoards cash during a recession, the economy slows to a crawl. That is the kind of economic suicide that Europe has leaped into: painful cuts, no growth, and rampant unemployment. America has avoided the worst of Europe’s fate thanks in part to the stimulus passed in 2009, and Japan, at last, looks to be hurtling in the opposite direction due to its recent stimulative policies. The key question is whether the pro-austerity politicians who currently control the purse strings in Washington and Brussels will take a hard look at the evidence accumulating around them — or retreat back into their comfortable, self-righteous views of the world.

John Maynard Keynes, the father of the proactive approach to economic policy that now bears his name, had something to say on this topic as well. Responding to a critic who questioned his shifting position on monetary policy during the Great Depression, the British economist answered: “When my information changes, I alter my conclusions. What do you do, sir?”

Ian Reifowitz Ian Reifowitz is the author of Obama’s America: A Transformative Vision of Our National Identity. Twitter: @IanReifowitz

- Follow us on Twitter: @inthefray

- Comment on stories or like us on Facebook

- Subscribe to our free email newsletter

- Send us your writing, photography, or artwork

- Republish our Creative Commons-licensed content